Inventory Costing Concepts: & Item model group - FIFO, LIFO etc, Microsoft Dynamic Supply Chain Management D365

Inventory Costing Concepts:

Why it’s important: Impact P/L, Drive Inventory Value, affect Margine. Cost of Sales is generally derived for Cost of Purchase and cost of production.

Basic inventory Flow - Create PO> Receive goods> Invoice goods> Customer place order > Ship goods.

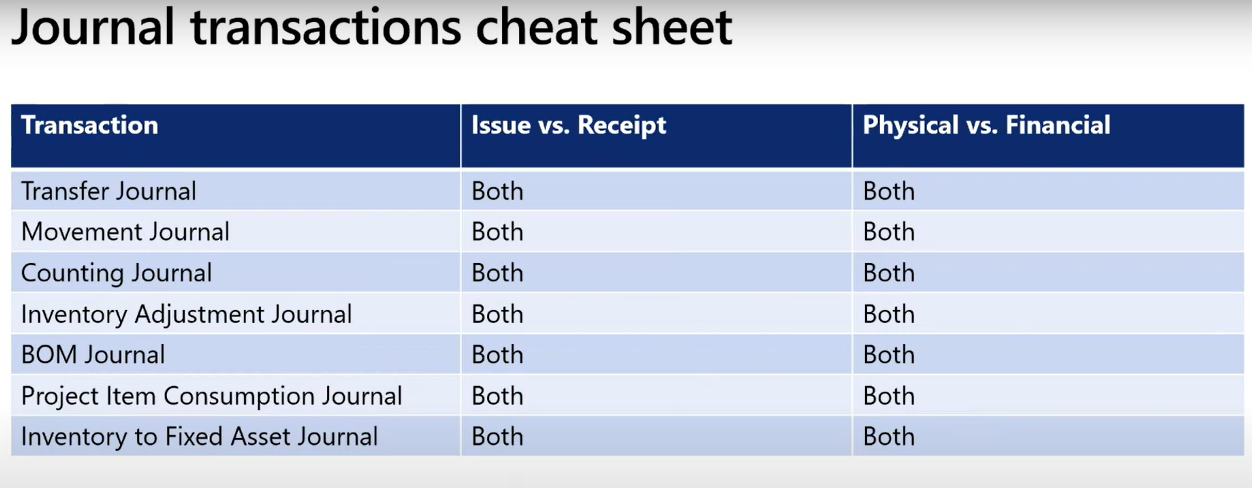

Inventory Status:

1.

Receipt Status: Order > Register

>Received Physical Update> Purchased Financial Update

2.

Issue Status: On Order> reserve

order>reserve Physical, Picked, > Deducted Physical update> Sold

Financial Update

Inventory Models:

1. Periodic – FIFO| LIFO| LIFO date |

Weighted average | Weighted average date.

2.

Perpetual – Moving average | Slandered

cost.

1.

Periodic Inventory Model: Issue use the

running average cost of on hand inventory.

2.

Perpetual Inventory Model: Transaction

post at the cost based on the cost model and do not get adjusted. Discrepancy

posted on a designated account. Marking doesn’t affect any cost to transaction. Moving average doesn’t need inventory closing.

Physical Negative Inventory = you are consuming more

then what you have. Despite no qty you can post the PO and warehouse will pick

the SO qty.

Dimension Group:

1.

Storage Dimension: Site, Warehouse, Location,

Inventory Status License Plate

2.

Tracking Dimension: Batch Number, Serial Number,

Owner

3.

Product Dimension: Style, Version,

configuration, Colour Size,

- FIFO

- LIFO

- LIFO dated

- Weighted average

- Weighted average dated

- Moving average

- Standard cost.

Let’s assume that a Suresh Ojha purchases 6 items for the cost of Rs 50 and 4 items for the cost of Rs 55. So,

the total items’ cost is 6*50 + 4*55 = 520

The company sells 4 items. Now,

there are 6 + 4- 4

= 6 items in the company warehouse.

So the possible cost of item remained in the warehouse are:

Possible Combinations:

(6 – 4) * 50 + 4 *55 = Rs 320 (The company has sold 4

items that cost Rs 50)

(6 – 2) * 50 + (4 – 2)

*55 = Rs 310 (The company has sold 2

item that costs Rs 50 and 2 item that costs Rs 55)

There will other variants

like 1 from Rs 50 and 3 from Rs 55, 3 from Rs 50 and 1 from Rs 55, etc.

We cannot come to the point

exactly about the item’s cost that is remaining in the warehouse because we

only know that there are 6 items remaining in the warehouse and we don’t know

which items are sold.

We can set up the following

rules for an inventory model to calculate item’s cost:

FIFO – First in First out. Means that the first purchased item is first sold.

So in our case, Suresh Ojha has 6 items for the cost of Rs 50 first, so these items will be first sold. After the items are sold, the items’ cost in the warehouse will be

(6 – 4) * 50 + 4 * 55 = Rs 320

LIFO – Last in First out. Meaning that the first purchased item is last sold.

So in our case, Suresh Ojha

has purchased 4 items for the cost of Rs 55 last, so these items will be first

sold.

After the items are sold, the items’ cost in the warehouse will be 6 * 50 + (4 – 4) * 55 = Rs 300

Weighted avg. In this case, the average cost is calculated and subtracted from the warehouse items’ cost when the item is sold.

So in our case, Suresh Ojha has average cost is (6* 55 + 4 * 50) / 10 =Rs 53.

After the items are sold,

the items’ cost in the warehouse will be (10 – 4) * 53 = Rs 318

Standard cost

This inventory model uses a specific price as cost. The price can be entered manually or calculated automatically. This price is used as cost for purchase and selling.

For example, if the Suresh Ojha has set the standard cost price of Rs 49. So, we purchase all items for this price Rs 49.

The total items’ cost before the selling is 6 * 49 + 4* 49 = 490. After 4 items are sold, the items’ cost in the warehouse will be (10 – 4) * 49 = 294.

LIFO date

This model equals to LIFO with the only difference being that purchase and selling dates are taken into account.

For example, a company purchases

4 items for the cost of Rs

50 on 11th Jan,

3 items for the cost of Rs

55 on 11th Jan

2 items for the cost of Rs 47 on 13th Jan.

The company sells two items on 11th Jan,

but the Sales manager was out

of office and didn’t post the sales. The Sales manager came back to the

office on 13th Jan and

posted the sales backdate to 11th Jan.

The sales posting process will decrease the cost of items in the warehouse at 2 * 55 (item’s last cost as of 11th Jan).

If the LIFO inventory model is used, the sales process will decrease the cost of items in the warehouse to 2*47 (because 7$ is the last cost received into the warehouse).

Weighted avg. date.

This model equals to the Weighted avg with the only difference being that the average amount is calculated for a separate day.

For example, a company purchases

4 items for the cost of Rs

50 on 11th Jan,

3 items for the cost of Rs

55 on 13th Jan

2 items for the cost of Rs

47 on 13th Jan.

The company sells two items on 13th Jan. The average cost price will be (3* 55 + 2 * 47) / (3 +2) = Rs 259.

Note: 4 items at the price of Rs 50 are not included in the average cost price calculation because they have been purchased on another day.

Costing Strategy:

Actual

Costing: FIFO| LIFO| LIFO date:

FIFO- Matches earlier issue transaction to the earlier receipt transaction.

LIFO-

Matches most recent receipt transaction against the earliest issue

transactions.

LIFO DATE- Matches most recent receipt transaction against the earliest issue transactions made on or BEFORE THE DATE of the issue transaction.

Average

costing (Common in retail industry) Weighted average | Weighted

average date| Moving.

average.

Weighted

average- Average cost of receipt for the PERIOD and applies as cost of all

issue.

Weighted

average date- Average cost of receipt for EACH DAY and applies that as cost of issue transaction for that DATE.

Moving

average- Use current average cost of physical receipts as final settlement price,

allow on hand inventory to be revalued.

Standard

Costing:

Slandered

cost:

Predetermined

cost used on every transaction. Based on past experience, typically set

annually.

Periodically

compared to actual cost.

To understand better how standard cost works, we need to understand the costing sheet.

Costing sheet.

Cost groups:

it’s a logical segmentation of total cost of an Item. Be it Direct material, packaging,

labor, Material, and overhead cost. Its also called as cost breakdown.

Note:

1.

If

you select on Direct material the cost group can only be assigned to released

product

2.

If

you select on Direct manufacturing the cost group can only be assigned to cost

categories. (Setup runtime)

3.

If

ITS undefined – they you can apply cost group anywhere you feel like.

4.

Direct

outsourcing is related to a service item.

Behavior

option on Cost group is – JUST to segments Fixed cost or variable cost.

Profit setting:

is just to increase the cost of BOM or Formulas by certain % on total

calculation – it also called as a total Sales Price of that item.

1.

Material-

Sourcing strategy, Type of material, overheads

2.

Labor-

Resource Type, Resource Cost, Overhead

3.

Indirect

cost- Calculation Method, Accuracy of overhead rates, Build vs Buy,

reconciliation.

Understand

the costing sheet.

Comments